Article by Somerset West Attorney - Nanika Prinsloo

The coronavirus will probably kill more businesses than people. The harm to the economy and the cost to businesses will be difficult if not impossible to calculate. According to Forbes business owners are fearful and worried about their future and drastic action is required to overcome these difficult times. This article will give you the legal information of some of these drastic actions that you can take to possibly get rid of the problem while you keep on trading.

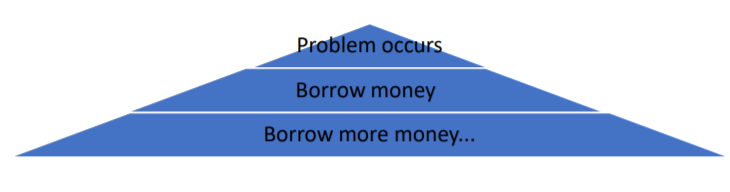

When a Business experiences financial or other pressure, the typical reaction of the business owner is to work harder to save the business or to try and trade out of the problem. They borrow more money, bond their houses, go smaller or bigger, sell assets, live more frugally and throw in everything they can to save the business.

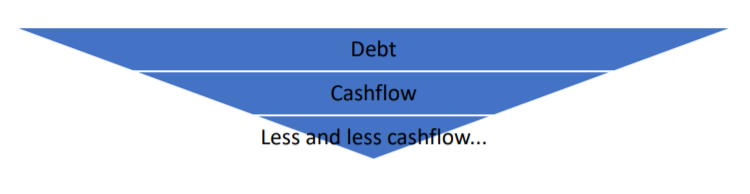

A small problem can cause you to borrow more and more money and you will end up with more debt… but the problem will still be there.

Some businesses have entered the pandemic with the above problem and the pandemic blocks cash flow which makes the service of debt impossible. The shutdown also brings other unique challenges that can affect healthy businesses.

A debt burden can paralyze you to such an extent that you may never recover financially. Restructuring and liquidation of your business can help you to get rid of debt and other potential problems so that you can keep on trading.

Restructuring can involve the liquidation of your business, the registration of a new company to enable you to continue to trade, we can arrange the buy-back of assets, re-visit how you do business, split divisions or deal with staff issues, etc..

Liquidation is just one of the tools we use in the restructuring process. It is an excellent mechanism to help you to reposition your business in such a manner that you can walk away from the problems but keep on trading with a fresh new start. If you signed personal surety, personal sequestration may be an option, alternatively, we should at least protect your assets.

Protection of Assets

If you have signed personal surety for the debt of the business, you will remain liable for the debt of the business even if you liquidate the business. If you are not going to personally sequestrate so that you can block the debt, then we need to protect your assets. You can buy back assets after liquidation so that the business can keep going, or you can do the same in the case of a sequestration. If you are not going to personally sequestrate, we need to protect your assets by, for example, transferring it to a trust. This only applies to assets that are fully paid. Assets that are under finance can only be attached by the financial institution that financed them if you do not keep on paying the instalments.

Sequestration

If you cannot pay your personal debt or any sureties that you signed for the business is too high, then we must look at your personal sequestration. Sequestration will block creditors from taking any legal action against you and, apart from about 25% of your debt, everything else will be written off (SARS debt included). Debt counselling is an option, yes, but you will still pay the debt, it will cost you a lot of money and you could find after five years of debt counselling you owe more than when you started….

Sequestration writes off all debt immediately and you never have to pay it back (except for approx. 25% of it). You remain under sequestration for four years and then you apply for rehabilitation that should get you back to normal.

Liquidation will let you lose your business to save it!

It is indeed possible to get rid of the debt in your Business by losing the Business through liquidation. In fact, you don’t stop trading at all (unless other reasons exist why you cannot or do not want to trade), but with careful planning and the appropriate legal advice, the only difficult part of the liquidation will be to make the decision to proceed.

If you need to keep going and your business is viable, we can put the structures (of which liquidation is one leg) in place that will enable you to do that. After a consultation with us, you will learn that liquidation is just a tool to use, it is not the end of the world. On the contrary, it is stopping your business from coming to an end.

In a liquidation, all the creditors “come together” (concursus creditorum) to share in the proceeds of whatever assets or monies the Business owns. If the Business owns nothing, then creditors will get nothing. They will, however, be part of the liquidation process and if they get nothing from the liquidation, then they must write the full debt off. If they get something, they must write the balances off. (if you signed personal surety you will remain liable for the debt. Any debt of the business you did not sign personal surety for will be written off.

The Master of the High Court appoints a liquidator after liquidation to wind up the insolvent estate of the business. While the liquidation process and the winding-up of the business take place, the business owner is left free to continue with his business if he wants to.

In terms of the Company Act, you must liquidate the business if it cannot pay its debt.

The classic mistake business owners make is to borrow money or bond their houses to put more money into the business to keep it going. This rarely works, because basically, unless something drastic happens that helps the business to trade out of its problem, the extra monies are basically just carrying the business. All you will be doing is juggle the books. The sooner you get rid of the problem and walk away, the better chance your business has to survive without having to throw good money after bad.

SARS is a creditor like any other and will become part of the liquidation. SARS stands about a third in line of creditors. It stands after the banks with bonds, landlords and the liquidator’s fees. If in the liquidation process, there are proceeds and it is sufficient to pay SARS, then SARS will get money, otherwise it will not. In my experience, for the last 10 years, SARS has never proved a claim against any insolvent business' estate and closed their file as soon as there is a liquidation.

Taxes owing in terms of the Customs and Excise Act are not written off after liquidation. It is the only taxes where the “manager of the premises”, in terms of the aforementioned Act, is held personally liable from the outset when the taxes occur.

Start the process. You are welcome to contact the writer of this article at nanika@nanikalaw.co.za or phone her at 072 8558 106